Abstract Future IC wafer foundry capacity and wafer demand forecast According to ICInsights' forecast, it is expected that the wafer manufacturing capacity of IC manufacturers will maintain a relatively rapid growth in the next few years, reaching 19.42 million pieces by 2018 and 2020 respectively. ..

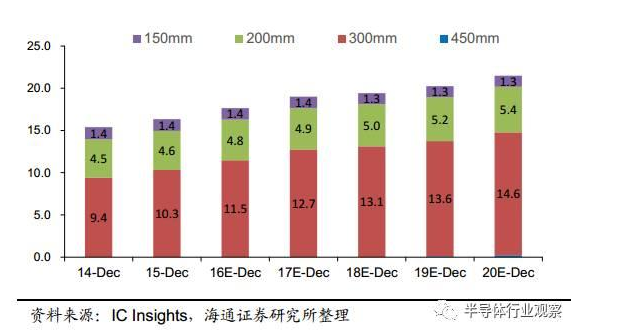

Future global IC wafer foundry capacity and silicon demand forecast According to IC Insights' forecast, it is expected that the wafer manufacturing capacity of IC manufacturers will maintain a relatively rapid growth in the next few years, reaching 19.42 million pieces and 21.3 million pieces (converted by 8 inch 200mm silicon wafers) by 2018 and 2020 respectively. With 863 and 9.47 million wafers on 12-inch wafers, the compound annual growth rate for 2015-2020 is 5.4%.

Global wafer monthly capacity from December 2014 to December 2020 (million pieces, 8 inch approx.)

As of the end of 2015, 12-inch (300mm) wafers accounted for 63.1% of global wafer production capacity, and the ratio is expected to increase to 68% by 2020. As for 8-inch wafers, the proportion of global wafer production capacity will be 2015. 28.3% will be reduced to 25.3% in 2020, but 8-inch (200mm) wafer capacity will continue to grow in the next few years; while 6-inch (150mm) wafer capacity will be relatively flat during the forecast period.

Global wafer monthly capacity share in December 2014-2020

According to SEMI statistics, global wafer shipments have increased rapidly over the past three years, from 8.852 billion square inches in 2013 to 10.269 billion square inches in 2015, with a compound annual growth rate of 7.7% from 2013 to 2015. It is expected that under the continuous investment of the mainland and Taiwan, it is expected that the foundry capacity will grow steadily, and Taiwan will be more stable in the region with the largest wafer foundry capacity in the world. Taiwan's foundry capacity ranks the highest in the world, with 12-inch capacity accounting for more than 55% of global foundry capacity. TSMC and UMC are the two drivers of Taiwan's foundry capacity. Taiwan Semiconductor Manufacturing Co., Ltd. 12-inch Fab 12 Phase 7, Zhongke 12-inch Fab 15 Phases 5 and 6 are actively preparing for production capacity below 10nm. UMC continued to expand its 28nm capacity, and Phase 5 of the Fab 12A plant at Nanke 12 Inch was also ready to invest in the 14nm process.

Mainland China will be the fastest growing market. According to IBS statistics, the scale of the foundry market in China in 2015 will be US$6.9 billion, and will reach US$15.4 billion by 2020, with a compound annual growth rate of 17.42%. The share of global foundry will increase from 9.3% in 2015 to 19.2% in 2020.

China's wafer foundry market size forecast (billion US dollars)

SMIC, the foundry leader in China, is currently working to increase the capacity of its existing plant in the 12-inch Fab B1 plant in Beijing and the Fab 8 plant in Shanghai's 12-inch plant. The company is also upgrading its newly established 12-inch Fab in Beijing. B2 plant and Shenzhen 8 inch factory Fab 15 plant capacity. SMIC's expansion plans include both advanced 28nm and 40nm capacity and a mature 8-inch wafer process; other expandable capacity companies include Wuhan Xinxin, which will continue to invest in NOR Flash foundry business; Shanghai Huali is also about to set up a second fab. It is expected to start construction in 2017, and it is expected to start betting capacity in the second half of 2018. With the development of advanced semiconductor process technology, the 28nm process has occupied the largest share in 2013-2015. It is expected that 28nm will remain the mainstream in the future, and from 2017, the more advanced 16/14nm and 10/7nm will grow rapidly. Advanced processes must be based on high purity, high quality silicon wafers.

In terms of specific industry applications, according to IHS's December 2016 report, it is estimated that from 2015 to 2019, calculations (including PC computers, SSD storage and tablets, 300mm silicon wafers), and industrial (200mm silicon wafers) The demand for wafers in the automotive and automotive sectors (close to 300mm and 200mm) will achieve a compound annual growth rate of 5%, 9%, and 6%, respectively, while the mobile phone field (mainly 300mm wafers) will be released due to shipments. The current demand will be maintained, but the proportion of 12 inches (300mm) will continue to increase.

Prediction of wafer demand growth in important semiconductor applications in 2015-2019

Overall, demand for 300mm wafers will continue to grow rapidly, and the number of 12-inch wafer fabs in global operations is expected to continue to increase by 2020. Most 12-inch plants will continue to be limited to producing large quantities of commodity-type components such as DRAM and flash memory, image sensors, power management components, and larger, complex logic and microprocessors for ICs; The foundry will combine orders from different sources to fill the capacity of the 12-inch fab. Current global semiconductor wafer production capacity

As we have analyzed in the previous article, from 2011 to 2013, due to the popularity of 300 mm large silicon wafers, the manufacturing cost per unit area of ​​silicon wafers decreased, and the competition for silicon wafer expansion was fierce. In 2013, the global market for silicon wafers was only 7.5 billion US dollars, falling for two consecutive years. In 2014, driven by the demand for automotive electronics and smart terminals, the price of 12-inch wafers rebounded and the global wafer market slowed down.

However, the wafer industry has been losing more and less in recent years, and major silicon wafer factories are unable to expand their production. Therefore, the global wafer production is growing slowly. From the low point of 2009, by 2015, global semiconductor wafer sales increased by 23.89%, and the compound annual growth rate was 3.63%. At the same time, global semiconductor wafer production increased by 58. 82%, compound growth rate of 8.02%, production growth rate exceeds sales growth, which also proves that the wafer industry is more difficult than the entire semiconductor industry.

If the market size (sales) is compared to the output, it can be defined as the average price of semiconductor wafers. It can be seen that it has remained at around US$0.77/sqm since 2013, compared to 1. The $46/sqm is greatly reduced.

Average global wafer price (USD/in 2 )

From the supply side, although the demand for silicon wafers began to recover, the production capacity has not changed much. According to SEMI data, by the end of 2015, the global 300mm wafer capacity was 5.1 million pieces/month. According to SUMCO, the demand for 300mm silicon wafers in the second half of 2016 has reached 5.2 million pieces/month. Under the premise that there is no large-scale expansion plan in the existing silicon wafer factory, the existing silicon wafer production capacity cannot meet the demand of silicon wafers. The global demand for 300mm wafers in 2017 and 2018 is expected to be 5.5 million/month and 5.7 million/month, respectively. At the same time, the growth rate of global silicon wafer production, according to SEMI's forecast, the compound growth rate in the next three years is about 2-3%, corresponding to 5.52 million pieces/month and 5.4 million pieces/month in 2017 and 2018. Supply shortage will be the norm.

2016-2020 Global Semiconductor Wafer Production Forecast (Million Square Inches)

In 2016, due to the demand for advanced processes such as 28nm, 20nm, 16/14nm, 3D NAND Flash, and the rapid growth of China's semiconductors, the global demand for 12-inch silicon wafer capacity increased significantly. The global semiconductor factory is launching a 12-inch wafer capacity competition, and demand for 12-inch silicon wafers is rising rapidly. At the same time, 8-inch wafers are also in short supply because of the gradual replacement of 8-inch silicon wafers by 12-inch in the past few years, resulting in a decline in the supply of 8-inch silicon wafers, but since 2015, automotive semiconductors, CIS sensors, and micro-control Demand for chips and other chips is growing rapidly, and many of these chips are still dominated by 8-inch wafers. At present, the capacity utilization rate of the first few wafer factories in the second half of 2016 is close to 100%. According to the announcement of Siltronic, the world's third largest wafer factory, the capacity utilization rate of silicon wafers in 2008 was only 60%, and from 2016. It has reached 100% since the beginning of Q3.

In the second half of 2016, Shin-Etsu, Sumco and Siltronic of the world's three largest silicon fabs announced that they will increase the price of the 112th silicon wafer in 2017 by about 10-20%, including TSMC, UMC, Micron (Micron). ) Semiconductor manufacturers are forced to pay.

According to Taiwan's authoritative media technology Times report, although TSMC has purchased a large number of silicon wafers, it has enjoyed more favorable prices than other customers in the past. However, due to the tight supply of 12-inch silicon wafers, TSMC has also been forced to reduce discounts. The magnitude is equal to the price increase in disguise; UMC has reported that the price of silicon wafers has increased by about 10-20%; Micron is preparing to invest heavily in 3D NAND Flash expansion, and its subsidiary Huaya Branch is also fully sprinting 20 nanometer DRAM capacity. The demand for adequate 12-inch silicon wafers has recently been reported to have been accepted by silicon wafer suppliers to increase the 2017 price by as much as 20%.

In the past few years, the semiconductor wafer industry has lost more and less. From the perspective of semiconductor wafer supply, the opportunities for expansion are still small. The losers are aiming at profit first. Companies such as SUMCO and Sunedsion hope that net profit will be Turn from negative to positive as early as possible. According to SUMCO's assessment, the construction of a semiconductor wafer factory with a capacity of 10,000 pieces per month and a capacity of at least 10 to 1.2 billion yuan will take 2-3 years from construction to production. Therefore, it is expected that the shortage of wafers will be in the next few years. It is the normal state.

According to the evaluation of the Taiwan Science and Technology Times, if the upstream raw material bare wafer price increases by 15%, it will inevitably affect the cost structure of downstream manufacturers. In the sales agent cost (COGS) structure of the foundry, the depreciation accounts for 50%. Bare wafers account for about 20% of the remaining 50%, so the price pressure is about 2 to 3%. Upstream suppliers are increasing prices, and companies such as TSMC will obviously transfer this price to OEM customers, and ultimately to consumers, which means that 2017 processors, NAND, memory, etc. are likely to continue to increase prices.

In summary, due to the loss of the semiconductor wafer industry in the past few years, from the perspective of the supply of semiconductor wafers, the opportunities for expansion are still small. According to SEMI data, the global 300mm wafer capacity will be 5.1 million pieces/month by the end of 2015. It is predicted that the compound growth rate of global semiconductor wafer production capacity will be around 2-3% in the next three years, corresponding to the production capacity in 2017 and 2018. 5.25 million pieces/month and 5.4 million pieces/month, but the demand for silicon wafers began to recover. According to SUMCO data, the demand for full 300mm wafers in the second half of 2016 has reached 5.2 million pieces/month, and the current 5.1 million pieces/month. The silicon wafer capacity cannot meet the needs of silicon wafers. It is expected that the global demand for 300mm wafers in 2017 and 2018 will be 5.5 million pieces/month and 5.7 million pieces/month, respectively. It will be normal to be in short supply.

Led Holiday Light,Outdoor Christmas Lights,Christmas Tree Lights,Led Christmas Lights

Yuyao Flylit Appliance Co.,Ltd , https://www.flylitlight.com